Income-Driven Repayment (IDR)

Important Note: On June 24, 2024, two court decisions temporarily blocked parts of the SAVE Plan from taking effect. These decisions may change borrowers’ rights and access to certain benefits, including repayment plans. We will update this website with more details on how this will impact borrowers soon. Visit here for more information.

Looking for an affordable student loan repayment plan? You may be eligible for an income-driven repayment plan, also known as an IDR plan. You can sign up for an IDR plan online, or by calling your loan servicer.

If you sign up for an IDR plan, you may qualify for payments as low as $0 per month based on your income. Plus, you can make progress toward having your loans forgiven (canceled) and being student debt-free on an IDR plan, even if your payment is $0 per month.

There are several different IDR plans, but all of them work in the same way: Your monthly payment amount is set each year based on your current income and family size and can go up if you make more money or down if you make less or your family grows. After a certain number of years of making payments, any loan balance you have left is forgiven (canceled). Beginning in 2026, there may be tax consequences for any loan debt that is forgiven through this program. See our page on IDR loan forgiveness for more information.

Click on each IDR plan below to see what may be the best option for you. You can also use the Department of Education’s helpful Loan Simulator Tool to see which of the plans you are eligible for and how much and how long you would likely pay under each plan to decide which is right for you.

Not sure which plan to choose? That’s ok! When you sign up, you can just check a box saying you want to be placed in the IDR plan with the lowest monthly payment, then there is no need to choose

Get one step closer to loan cancellation through the IDR account adjustment!

The Department of Education recently announced a one-time account adjustment to help borrowers get more credit toward IDR and PSLF loan cancellation. While most borrowers will get this credit automatically, some borrowers may have to take steps before June 30, 2024 to receive this credit. Don’t miss out. See our IDR account adjustment page for more information.

The SAVE plan is the newest IDR plan, and it will replace the current REPAYE plan. Some of the SAVE Plan benefits are being implemented early in September 2023, but many benefits won’t go into effect until July 1, 2024. If you are already enrolled in the REPAYE plan, you will be automatically transferred to the SAVE plan before July 2024.

Parent Plus Loans or Direct Consolidation Loans that paid off Parent Plus loans are not eligible for SAVE.

Your monthly payment is based on your income and family size. If you make less than 225 percent of the Federal Poverty Line for your family size, you will have a $0 monthly payment. Until July 1, 2024, if you make more than 225 percent of the federal poverty line, your monthly payments will be 10 percent of the portion of your income above that amount.

After July 1, 2024 if you make more than 225 percent of the federal poverty line, and you only borrowed loans for your undergraduate education, your monthly payment will be 5% of any income above 225 percent of the federal poverty line

If you only borrowed loans for graduate school, your monthly payment will be 10% of your income above 225% of the federal poverty line. If you borrowed for both graduate and undergraduate schools, your monthly payment will be a weighted average of your loans and will be between 5% and 10% of your monthly income above 225 percent of the federal poverty line.

You have to recertify (update) your income and family size each year, even if they haven’t changed. If you’re married, you and your spouse’s income and student loan debt will not be considered together to determine your payment if you file your taxes separately (with limited exceptions).

One of the biggest benefits of the SAVE Plan is that the Department of Education will stop charging you interest that is not covered by your SAVE plan payment. This means that unlike other IDR plans, you will not see your total loan balance increase while making payments in the plan.

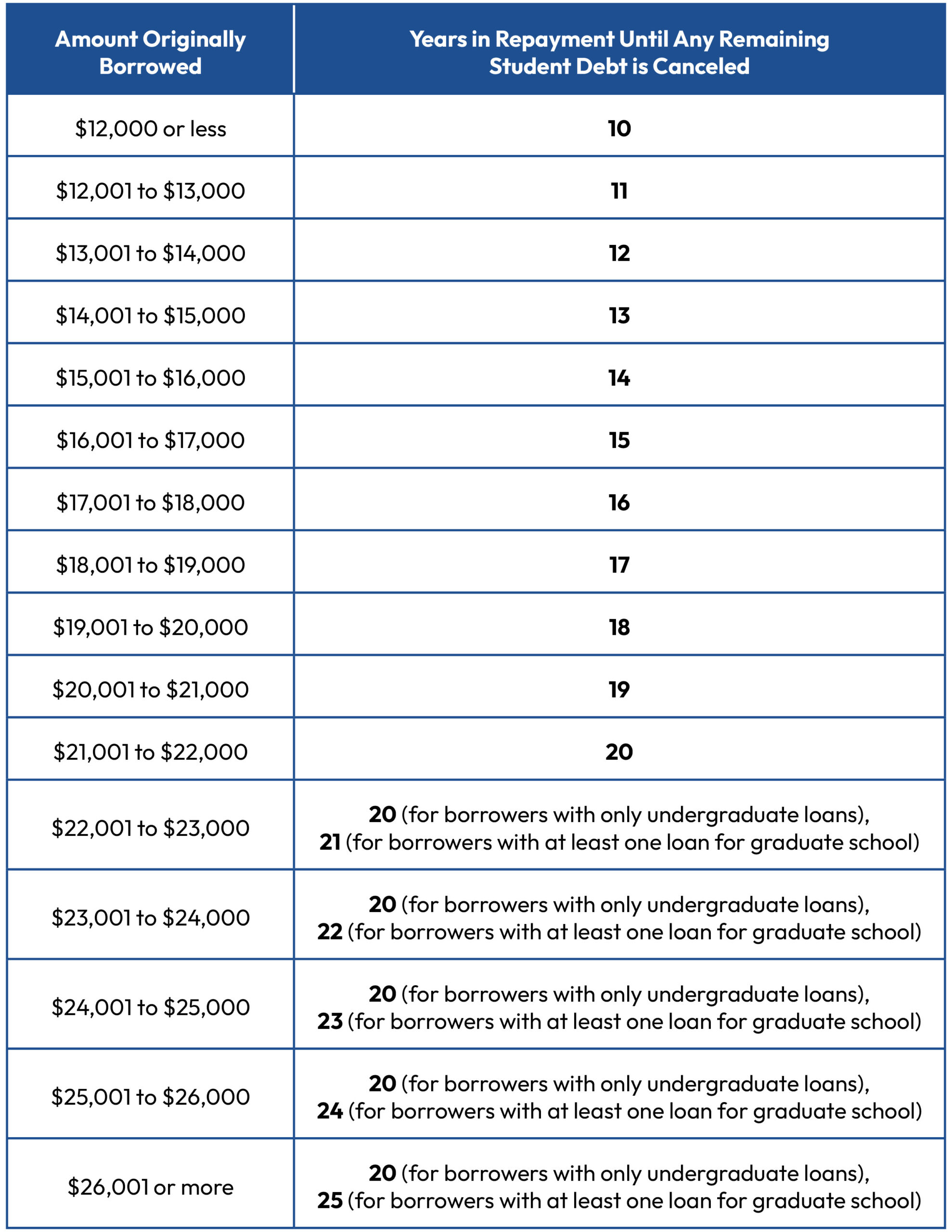

If you continue to make payments under SAVE, any remaining balance on your loans will be canceled after:

See the chart below and our blog post on this issue for more information on when you may be eligible for cancellation under the SAVE plan.

Depending on your income and debt, you may pay off your loans sooner. See our blog post for more information on the SAVE plan, including information about who is eligible for a $0 payment!

The REPAYE plan is being replaced by the SAVE plan. The REPAYE plan will be fully replaced by the SAVE plan in July 2024. If you are already enrolled in the REPAYE plan, you do not have to take any steps to enroll in the SAVE plan. You will be automatically transferred to the SAVE plan before July 2024. No one new can enroll in REPAYE now, but you can enroll in the SAVE plan.

Parent Plus Loans or Direct Consolidation Loans that paid off Parent Plus loans are not eligible for REPAYE.

Your monthly payment is based on your income and family size. Payments are 10 percent of your monthly discretionary income (defined as the difference between your income and 150% of the poverty guideline). You have to recertify (update) your income and family size each year, even if they haven’t changed.

If you continue to make payments under REPAYE, any remaining balance on your loans will be canceled after:

Depending on your income and debt, you may pay off your loans sooner.

The following types of loans are eligible for PAYE if the borrower meets other eligibility requirements:

Parent Plus Loans or Direct Consolidation Loans that paid off Parent Plus loans are not eligible for REPAYE.

In addition, you are only eligible for PAYE if your payment in PAYE would be less than your payment in a Standard plan and if you received a Direct Loan on or after October 1, 2011 and you had no outstanding Direct or FFEL loan balance when you received your first federal loan on or after Oct. 1, 2007. Most newer borrowers meet these criteria.

Your monthly payment is based on your income and family size. Payments are 10 percent of your monthly discretionary income (defined as the difference between your income and 150% of the poverty guideline), but will never be higher than what you would pay under the 10-year Standard repayment plan.

You have to recertify (update) your income and family size each year, even if they haven’t changed. If you’re married, you and your spouse’s income and student loan debt will be considered to determine your payment only if you file your taxes jointly. If you file your taxes separately, only your information is used to determine your payment.

If you continue to make payments under PAYE, any remaining balance on your loans will be canceled after 20 years of payments. Depending on your income and debt, you may pay off your loans before 20 years.

All Direct and FFEL Loans are eligible for IBR, except for Parent PLUS loans and Direct Consolidation Loans that repaid Parent Plus loans.

In addition, you are only eligible for IBR if your payment in IBR would be less than your payment in a Standard plan

Your monthly payment is based on your income and family size and depends on when you borrowed:

In IBR, just like in PAYE, payments will never be higher than what you would pay under the 10-year Standard repayment plan.

You have to recertify (update) your income and family size each year, even if they haven’t changed. If you’re married, you and your spouse’s income and student loan debt will be considered to determine your payment only if you file your taxes jointly. If you file your taxes separately, only your information is used to determine your payment.

If you continue to make payments under IBR, any remaining balance on your loans will be canceled after:

Depending on your income and debt, you may pay off your loans before you reach 20 to 25 years of payments.

IBR is generally the only income-driven repayment plan available to borrowers with FFEL loans. But PAYE or REPAYE may be a better option for Direct Loan borrowers. If you have a FFEL loan and want to sign up for an IDR plan, you may want to consider consolidating your FFEL loan into a new Direct Consolidation Loan to qualify for PAYE or REPAYE. See our page on consolidation for more information.

FFEL loans and Parent PLUS loans that have not been consolidated are not eligible for ICR.

ICR is the only IDR plan that is available to borrowers with Parent Plus Loans, but you first have to consolidate your Parent PLUS loan into a new Direct Consolidation Loan to be eligible. For more help, see our page on consolidating loans.

Your monthly payment is based on your income and family size. Payments are capped at 20 percent of your monthly discretionary income (defined for ICR as income over 100% of the poverty guideline), though may be lower based on a complicated alternative formula.

You have to recertify (update) your income and family size each year, even if they haven’t changed. If you’re married, you and your spouse’s income and student loan debt will be considered to determine your payment only if you file your taxes jointly. If you file your taxes separately, only your information is used to determine your payment.

If you continue to make payments under PAYE, any remaining balance on your loans will be canceled after 25 years of payments. Depending on your income and debt, you may pay off your loans before 25 years.

ICR is generally the most expensive IDR plan, but it is the only plan available for borrowers with Parent PLUS loans or Direct Consolidation Loans that repaid Parent PLUS loans. ICR is not generally recommended for anyone except for Parent PLUS borrowers.

Need more help choosing an IDR plan?

You can use the Department of Education’s free Loan Simulator Tool to compare repayment plans and decide which plan may be right for you.

If you disagree with how your loan servicer calculated your IDR payment after you applied, contact your servicer. It’s possible they made a mistake. You may also be able to switch plans to get a lower monthly payment amount if there wasn’t a mistake. If you still think the payment amount is wrong, you can file a complaint with the Federal Student Aid Ombudsman.

The National Consumer Law Center (NCLC) shares stories about borrower issues with lawmakers and policy advocates on a regular basis. Share your story and help us fight to make the law better for borrowers!